“In my experience, there’s no such thing as luck.”

– Obi-Wan Kenobi, Star Wars

The unofficial end of summer is upon us, and save for a few fleeting days of volatility, it was a fruitful season for diversified investors. Even so, a few storm clouds have begun to descend, with unemployment rising and earnings revisions turning mildly negative.

But last week’s clear and dovish remarks from Fed Chair Jerome Powell may have given investors a new hope that easier policy can still “Force” a soft landing. The world’s most powerful central banker said “the time has come” to lower policy rates and that he won’t tolerate any further softening in the labor market. But that’s not the only thing we have to look forward to into year end. As many families prepare for their last weekend of the summer, we’re preparing for an eventful final four months of 2024.

“This station is now the ultimate power in the universe.” – All Eyes on the Fed

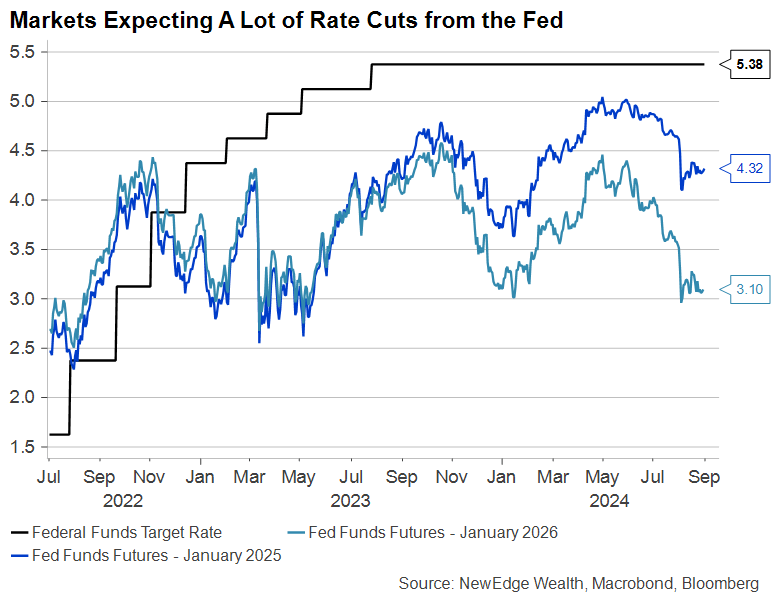

With the 2Q24 corporate earnings season winding to a close, central banks and the economic data that inform their decisions will dominate market behavior. Chair Powell’s comments in Jackson Hole last week confirm that the Fed will join its rate-cutting peers around the globe, with inflation risks receding and concerns about the labor market beginning to simmer.

How much will the Fed ultimately cut rates? Judging by futures prices, investors seem to imagine quite a bit. The Fed’s own estimate of a “neutral” rate, the policy rate that is considered neither stimulative nor restrictive to economic growth, is currently between 2.5% and 3.0%. Investors are expecting the committee to cut rates close to that range by the end of next year. Whether this market forecast is correct will depend on how much the economy slows in the coming quarters. The question about how much the Fed could cut this cycle is a topic we will dive into greater detail in next week’s Weekly.

“I have a bad feeling about this.” – A Murky Employment Picture

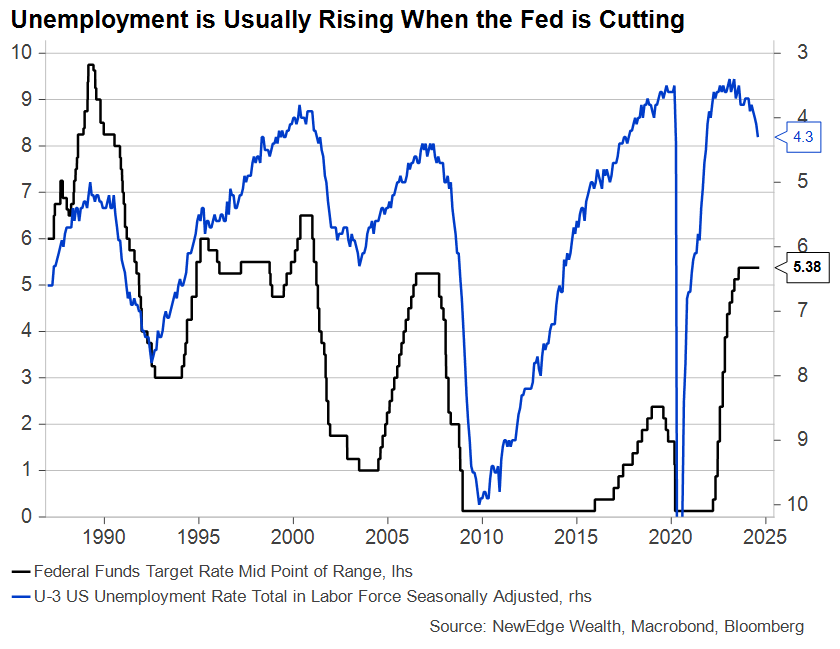

While we wait to see whether the Fed cuts by 25 or 50 bps in a few weeks (the market currently sees a 30% probability that the Fed will do a supersized 50 bps cut), we are growing more concerned about the U.S. labor market. Like the Millennium Falcon approaching the Death Star, we are watching for risks that the labor market may be caught in a tractor beam that could eventually pull the unemployment rate to 5% or higher.

History suggests that it may already be too late to avoid that fate, as Fed rate cuts will do little to strengthen hiring in the short run, given uncertainty about the growth trajectory and policy environment in 2025.

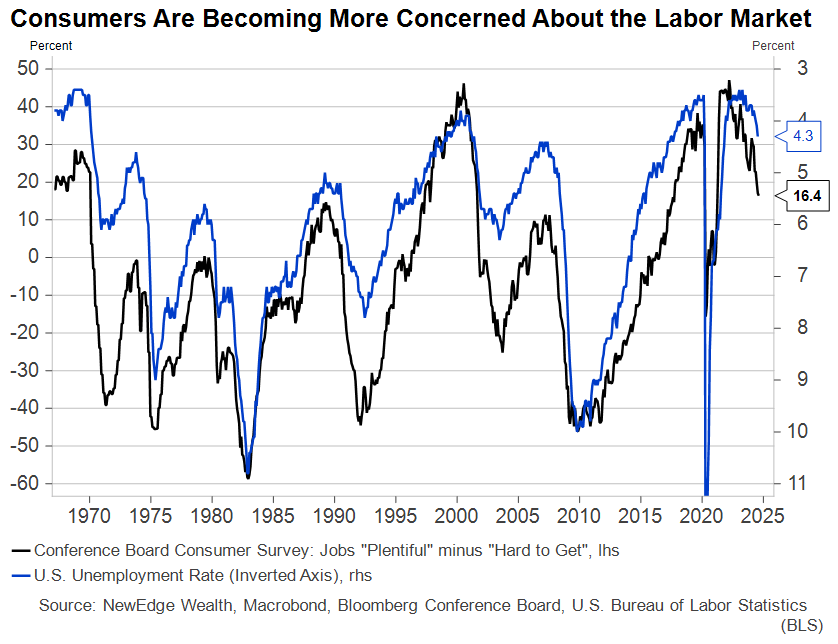

This week brought more worrying news on consumer attitudes about the labor market. While sentiment surveys have become unreliable predictors of consumer spending, respondents’ views on job availability have generally been a reliable indicator about the state of the labor market.

The number of people who see jobs as plentiful has been falling while the number who consider them “hard to get” has been rising. The spread between these two attitudes, often referred to as the Labor Market Differential, typically narrows as unemployment rises.

Looking forward, the key question will be if the slowdown in hiring will be followed by an uptick in firings/layoffs. Slower hiring typically is followed by higher layoffs and, thus, a rise in unemployment, but nothing has been typical about this Strange cycle.

On the bright side, the recent dovish turn in public Fed comments may convince employers in rate-sensitive industries that significant layoffs are not necessary, meaning a sharp rise in joblessness may yet be avoided. The layoff rate remains historically low, but if it does rise from here, it could mean a recession is at our doorstep.

“Uh…everything’s perfectly all right now. We’re fine.” – Complacent Credit Markets

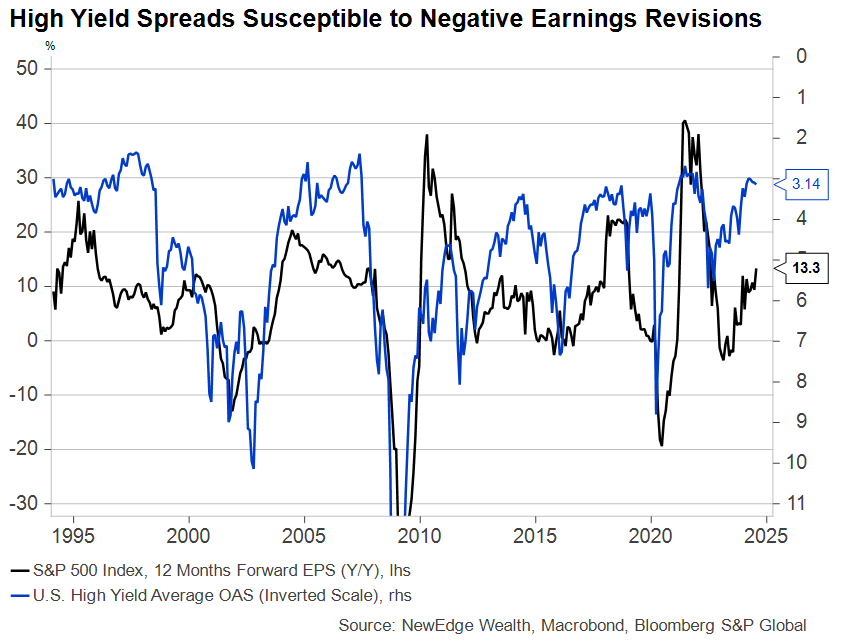

When volatility spiked earlier this month, spreads on corporate bonds widened abruptly, calling attention to their macro sensitivity and the “priced for perfection” valuations that credit reached through the early summer rally. Indeed, credit has a reputation for acting as a canary in a coal mine during times of slowing economic and earnings growth.

For now, credit markets appear to be breathing a sigh of relief as the growth scare abates, but given the return of high valuations, any wobble in the earnings outlook from here would likely trigger a widening of spreads that could offset a drop in underlying rates.

We remain underweight, low-quality credit in our fixed income strategies even as we expect it to perform solidly in our base case. Asset allocation is about being paid for the risk you are taking, and junk credit is simply not valued attractively for the risk it would present to portfolios in a downturn.

“This bickering is pointless!” – The November Election Looms

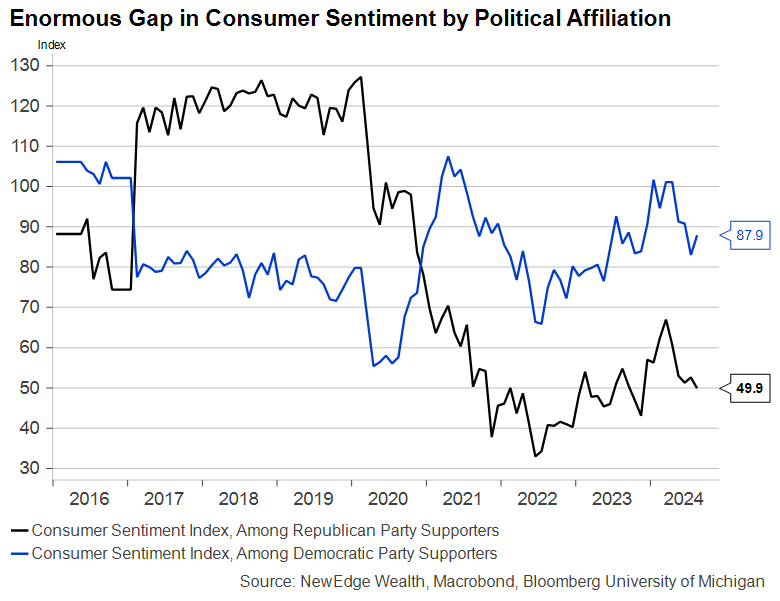

With Fed rate cuts almost certainly a “go” for the rest of the year, the U.S. election has now become the main source of policy uncertainty in our 2025 outlook. Investors can fall prey to overrating the importance of politics – and political alignments – to the performance of the economy and the markets. We see this in consumer confidence surveys every time there’s a change in leadership, as seen in the sharp changes in consumer sentiment levels from each party following recent elections.

The distribution of policy outcomes in 2025 is likely not as wide as the range of policy proposals officially on the table from the two major presidential candidates. Both the Senate and the House are likely to be governed by very thin majorities, regardless of which party ultimately controls them. And most sweeping legislation requires 60 or more Senators – not an easy tally even in the most tranquil of times – to pass.

The exception to this rule is changes to the tax code, which can be done through budget reconciliation using a simple majority. This will be the most likely channel for major policy changes, particularly given the expiration of many provisions of the 2017 Tax Cuts and Jobs Act in January 2026. There will be considerable fiscal policy uncertainty even after the election outcome is known.

We are also watching for potential policy changes that could be done through the Executive branch, without having to go through Congress, such as tariff policy.

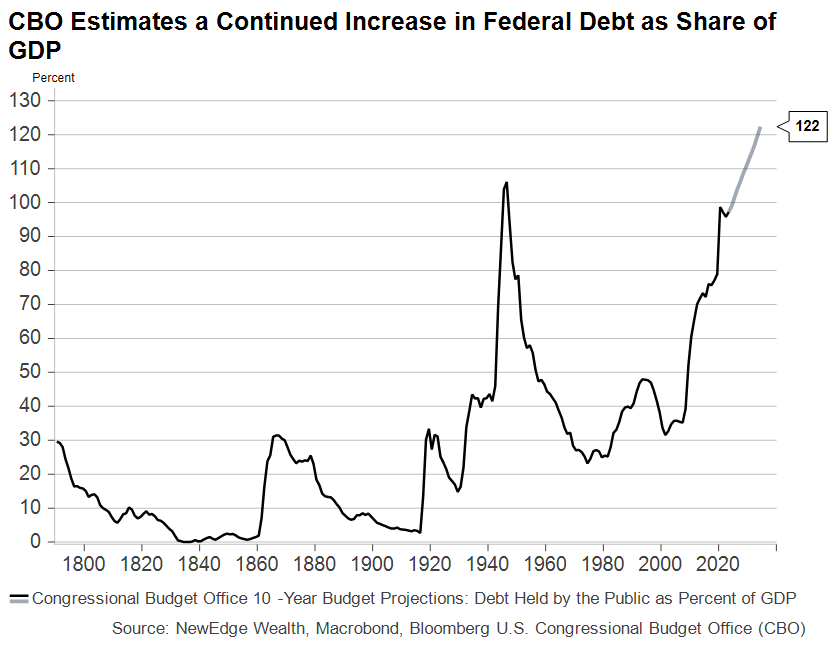

Depending on the outcome of the election, particularly at the presidential level, all aspects of the tax code will be on the table as politicians look for a way to enact their preferred policies without further exacerbating the alarming federal debt picture. Individual income taxes account for the lion’s share of revenues, but who is taxed – and how…and by how much – will depend on party alignment and the priorities of the new president.

We will have more to say on the election and the issues it raises for investors in the coming weeks.

Conclusion: Fed Not Quite Our Only Hope, but We Could Use Its Help Just the Same

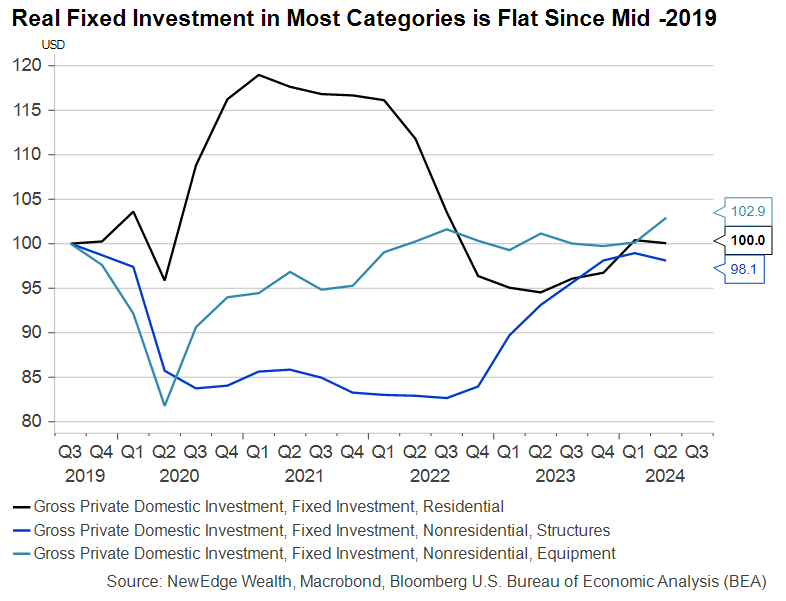

Less restrictive monetary policy is a necessary but insufficient condition to avoid an economic downturn in 2025. Lower rates could boost activity in segments of the economy – particularly those connected to investment – that have experienced little if any real growth, on net, over the past five years.

Monetary policy works with a long lag, but we know markets have a new hope that easier conditions lie ahead. Will this be enough to reverse the path of recent easing in labor markets? It remains to be seen and may be one of the most important questions for 2025.

[dipl_divi_shortcode id=”40772″]