Introduction: A New World for a New Fed

“There’s a button for that.”

A lot can happen in a week, and the past week was notable in three ways. First, the U.S.-Iran conflict appears to have reached the beginning of its end, with both sides expected to sign a Memorandum of Understanding (MOU) to bring about an end to hostilities (and blockades) and begin negotiations. Second, new Fed Chair Kevin Warsh led his first meeting of the Federal Open Market Committee (FOMC). In a distant third came a slew of U.S. economic data, some but not all of which came in below expectations. Together, these developments further cloud the outlook for the economy over the balance of 2026 and may make the opening months of Chair Warsh’s tenure difficult to navigate.

Warsh’s confirmation process was controversial, coming as it did during a period of unprecedented attacks from the president on the former Fed Chair. From the beginning, however, we have not believed his decisions once in the role would be overly influenced by political considerations. His first press conference, promising major changes and a return to first principles, seemed to affirm our view. To that end, our offering this week will draw heavily from the 2021 Ryan Reynolds film Free Guy, in which a “non-playable character” in a popular online roleplaying game suddenly (thanks to AI) gains agency…and popularity.

Don’t Have a Good Fed Day. Have a Great Fed Day!

“I know this world is just a game, but this place, these people, that’s all I have.”

Even without the debut of a new Fed Chair announcing big changes (as Warsh did), the June FOMC meeting would have been notable in several ways. First, the FOMC has become more rambunctious lately, with dissents becoming more routine and individual regional presidents and governors striking out on their own to comments on inflation and the appropriate path of policy. The Fed’s new communication strategy, clearly spearheaded by Warsh himself, is to say less in its statements about its plans going forward or what would make it change its policy rate target. Phrases like “In considering the extent and timing of additional adjustments to the target range for the federal funds rate…” which was in the April statement, are now absent. This probably made it easier to achieve unanimity, as most FOMC members can agree on statements of fact rather than opinions about the proper path of policy moving forward.

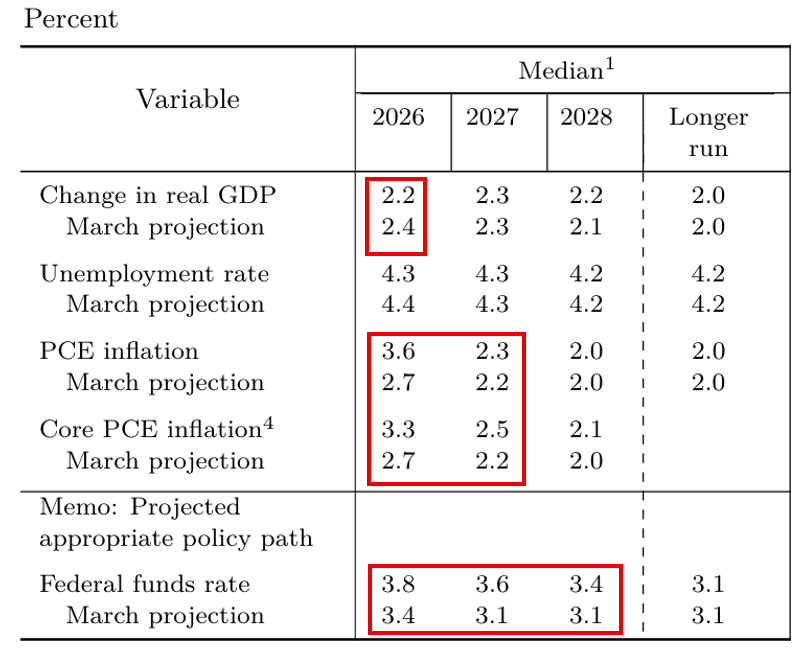

Second, thanks to the conflict in the Middle East, the U.S. economy has experienced a major economic shift since the March meeting, which led several forecasts to be revised dramatically:

Source: Federal Reserve, as of 6/17/26

The economic forecast revisions once again had the whiff of stag-flation, with 2026 GDP growth revised down to 2.2% while expectations for inflation soared to well over 3% for both headline and core PCE prices. Perhaps most notably, the median forecast for core PCE inflation for 2027 also rose by 0.3% to 2.5%, a rate most of the FOMC would deem to be unacceptably high.

The absence of forward guidance from the FOMC statement seemed to give the members’ “dot plots” greater importance for markets. The dot plot itself also had a hawkish tilt, with just one “dot” reflecting a single interest rate cut in 2026 (this wasn’t Warsh; he declined to submit a forecast) while exactly half of the dots (nine) called for one or more hikes. The rest of the committee felt leaving rates on hold would be appropriate. Compared to the March projection, the FOMC has added 0.375% to its 2026 expectations for the policy rate and 0.5% to its 2027 expectations. That is still not as high as the market expects, but the gap has shrunk considerably.

Do Lower Oil Prices Make the Fed’s Job Easier or Harder?

“Life doesn’t have to be something that just happens to us.”

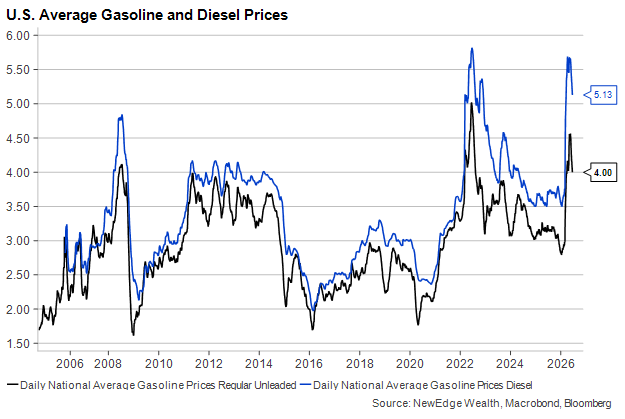

It’s hard for us to imagine a geopolitical event that could confuse a central bank more than a monthslong disruption to global oil supply. To wit, the European Central Bank last week elected to raise its policy benchmark rate for the first time since 2023. Europe’s economy has not grown for two quarters, and core CPI inflation on the continent has only been 2.6% over the past year. In tightening policy, the ECB is effectively attempting to dampen inflation in parts of the economy it can control (e.g., housing) to offset higher inflation in the part of the economy (e.g., gasoline prices) that it cannot.

As of 6/17/26

It seems unlikely to us that the Fed will go down a similar path, especially with oil supply (supposedly) about to be slowly restored to normal and gasoline prices falling quickly, as the graph above shows. What has become clear, however, is that the surge in energy-driven inflation during the first half of this year is going to prevent the Fed from cutting rates anytime soon. It’s easy to forget now, but rate cuts – on a mix of weaker hiring and moderating inflation – was the Fed’s plan heading into the year.

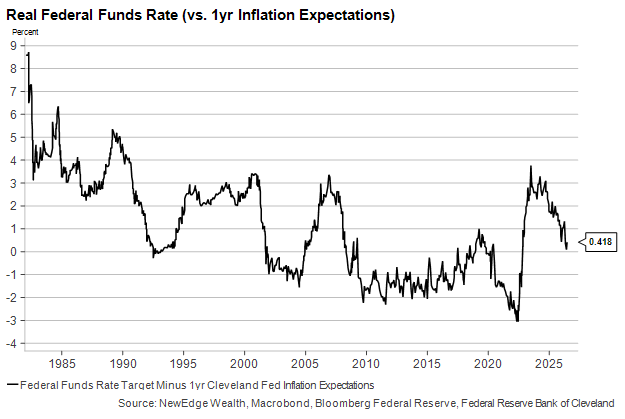

Fortunately, the labor market’s recent stabilization makes the conversation about cutting rates less pressing for now. Financial market conditions are loose enough to support tight credit spreads, high equity valuations, and, it seems, at least an occasional $2 trillion IPO. The Federal Funds Rate is only slightly higher than the Cleveland Fed’s 1-year Inflation Estimate, and it’s well below realized headline inflation over the past year:

As of 6/18/26

When asked how he felt about the “hawkish” set of forecasts his colleagues submitted last week, Chair Warsh noted that the projections seem to have been written in pencil. This underscored both his skepticism about economic forecasting, in general, and a more specific view that delivering guidance on the economy or rates is unusually challenging right now. We happen to agree.

No Signs of Political Interference Here!

“I want to comply! I just find the order of those threats very confusing.”

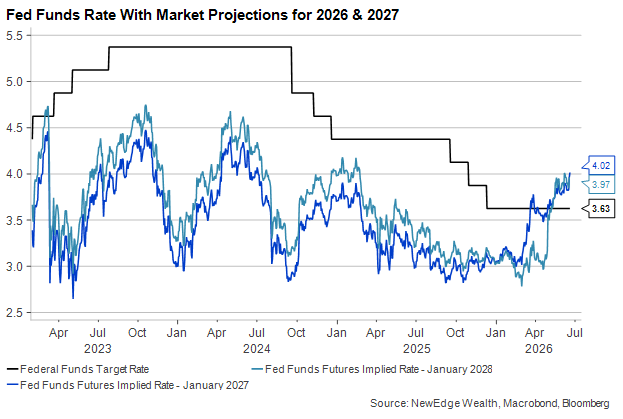

Judging by Chair Warsh’s refusal to provide guidance to markets on the direction of monetary policy (heck, it was hard to even get him to deliver a frank assessment of current conditions at his press conference last week), he probably does not care much that markets are pricing in earlier rate hikes following the Fed’s June meeting. But they are:

As of 6/18/26

Warsh’s approach for the next six months will be to start from scratch with the Fed’s approach to interpreting data, communicating with the public, and managing its balance sheet. He did note that changing the Fed’s 2% inflation target will not be on the table, a move no doubt designed to solidify the Fed’s hard-won credibility on delivering price stability. The mere belief among investors that inflation will eventually get back down to 2% makes delivering on that promise much easier (which is why the Fed has so frequently discussed the “anchoring” of inflation expectations).

On that point, the gap in yields between the 2-year and 10-year U.S. Treasury Notes shrunk sharply on Wednesday, which typically happens when monetary policy is tightening (i.e., short-term rates rising more than longer-term rates). This is another sign that markets do not view politics as a factor in monetary policy and are not demanding much of a premium to lend to the U.S. Treasury for longer time periods.

As of 6/18/2026

Conclusion: What Could Go Wrong?

“Now maybe that’s just my programming talking, but guess what? Somebody wrote that program.”

The risk for any new Fed Chair is a significant macro or market shock. Warsh’s approach to the job will be to allow markets to react to events and data rather than to guess how the Fed will react to them. That is a worthy and admirable goal. But should a market crisis arise, even one that is not of the Fed’s own making, investors will want to understand how and how much the Fed is committed to help in the form of rate cuts and liquidity injections.

We do not expect a “moment of truth” in which the Fed must decisively either tighten or loosen monetary policy to pop up this year. But we can easily imagine scenarios in which inflation roars higher (due to a resumption in Middle East hostilities, say) or the jobs market starts to soften with consumers getting squeezed.

Perhaps the Fed has overcommunicated and overpromised during the past three Fed Chairs’ tenures, and Warsh’s chairmanship will be a needed correction from the central bank’s tendency to talk more, write more and do more. But the transition between the Bernanke/Yellen/Powell approach and the new one could be rocky, at least at the outset.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC

The post A Man of Few Words appeared first on NewEdge Wealth.