This week, we shared our outlook for the economy and markets in the second quarter of 2024.

Below you will find the link to the whole, detailed slide deck.

For those who would like a quick summary, the deck includes the following key takeaways:

• Economy: We expect broad U.S. economic data to remain resilient in the second quarter. There are signs of incremental strength in the economy, such as in manufacturing, while also signs of incremental weakness, such as in peripheral labor data (job openings, hours worked, etc.). After a large increase in 2024 GDP estimates (from 1.2% to 2.2% over the course of the first quarter), we do not see as much upside to GDP estimates from here. We are watching for signs of continued inflation stickiness that have emerged in recent months, keeping a close on commodity markets.

• Fed: If data resilience continues, we expect the Fed and the bond market to continue to moderate rate cut expectations for 2024, as we see 1-2 cuts maximum in a robust growth environment (but continue to note that in the last 40 years, the Fed has never started a rate cutting cycle when manufacturing Purchasing Managers Indices were rebounding, as they are currently).

• Fixed Income: We expect continued upward pressure on yields from stronger economic data, stickier inflation, the prospect of a tighter Fed, and, potentially, Treasury supply dynamics. Higher long yields can eventually present buying opportunities. We watch for deterioration in economic data to be the source of yield downside. In credit, strong economic growth keeps credit fundamentals solid, but note that given how tight credit spreads are, along with increased issuance, any weakness in growth outlooks could cause brisk spread widening.

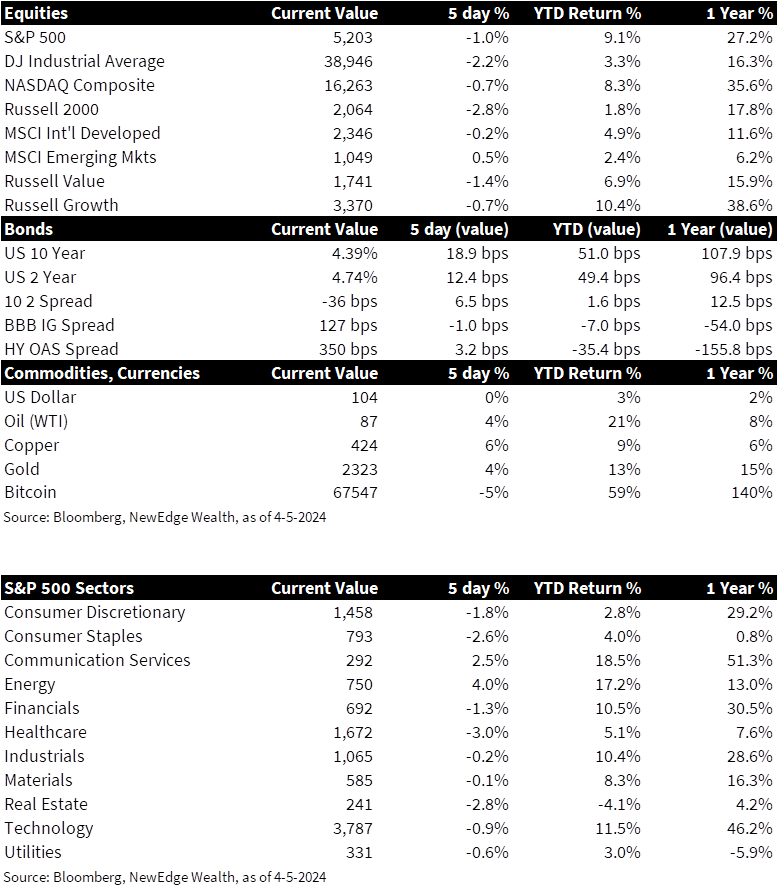

• Equities: We expect the second quarter to be marked by higher volatility compared to the first quarter’s ultra-low volatility rally. High multiples, crowded positioning, and ebullient sentiment can be tolerated by markets as long as growth forecasts continue to rise and liquidity stays abundant. However, if growth estimates are trimmed or liquidity recedes, we could see a bout of volatility that can be used as an entry point for underweight investors. We expect the rotations that began in late 1Q24 to continue into 2Q24 (which has been led by cyclical Value sectors like Energy, Materials, Industrials, and Financials). We watch the Technology sector closely, as its continued strength is critical for the overall market given its large weight in the index (meaning Tech can lag, but it cannot be weak for overall market returns).

• Alternatives: We continue our cautious optimism and highly selective approach to alternatives, noting structural shifts in the operating background for important asset classes like Private Equity and Private Credit that demand investors to be discerning.

For much, much more detail, please click here for our complete analysis of the second quarter macro and market environment.

IMPORTANT DISCLOSURES

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. Dow Jones Industrial Average (DJ Industrial Average) is a price-weighted average of 30 actively traded blue-chip stocks trading New York Stock Exchange and Nasdaq. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. Russell 1000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The BBB IG Spread is the Bloomberg Baa Corporate Index that measures the spread of BBB/Baa U.S. corporate bond yields over Treasuries. The HY OAS is the High Yield Option Adjusted Spread index measuring the spread of high yield bonds over Treasuries.

Sector Returns: Sectors are based on the GICS methodology. Returns are cumulative total return for stated period, including reinvestment of dividends.

[dipl_divi_shortcode id=”40772″]